By Vishal Gupta

International Financial Reporting Standards (IFRS) set common rules so that financial statements can be consistent, transparent and comparable around the world.

The International Accounting Standards Board (IASB) is an independent and privately funded body that develops and approves International Financial Reporting Standard (IFRS) standards. Prior to 2003, standards were issued as International Accounting Standards (IASs). In 2003, IFRS 1 was issued and all new standards are now known as IFRS standards.

The IFRS Foundation has currently 22 Trustees who monitor and fund the IASB, IFRS Advisory Council and IFRS Interpretations Committee.

Advantages of IFRS Standards

- Ensure Global presentation & makes comparison easier with foreign competitors.

- Facilitation of Cross border transactions, easier to raise capital abroad.

- Number of potential Merger and Acquisition deals across countries widens up.

Disadvantages of IFRS Standards

- Cost of first-time adoption and further implementation.

- Rumors and comparison of having low level of detailing as compare to US GAAP.

ADOPTION OF IFRS IN INDIA

Ind AS stands for Indian Accounting Standards and are converged standards for IFRS. To ensure India converge globally accepted standards, IFRS, Ind AS were adopted and are being mandatory for certain companies.

IFRS 1- First Time Reporting of International Financial Reporting Standard

It shows path to entities for applying IFRS Standards for the first time.

Issues to be taken care of:

- Transparent for stakeholders and comparable across all periods.

- Cost of adoption should not exceed potential benefits of adoption.

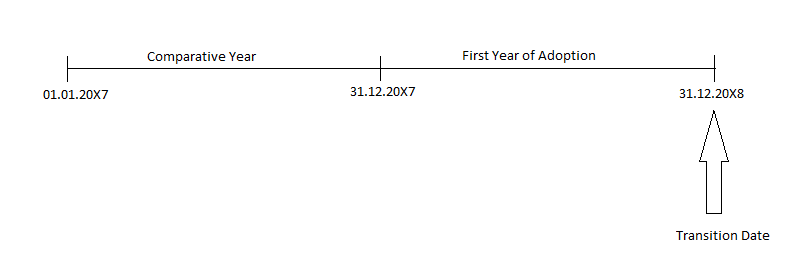

Transition Date:

The date on which IFRS standards has been implemented for the first time. A company adopting IFRS standards for the first time will be required to present the immediate previous year financial statements according to IFRS standards for Comparison Purpose.

Example:

Adjustments are supposed to be recognized directly in Retained Earnings, not in Statement of Profit and Loss.

Important Concerns during Transition Period:

- Derecognize the existing asset and liabilities and recognize new asset and liabilities as per respective IFRS Standards.

- Fair Value Measurement of exiting asset and liabilities according to IFRS.

- Cumulative Translation Differences on foreign operations required to be dealt.

- Consolidation of parent’s financials with subsidiaries, associates and joint ventures.

Disclosures Required:

- Reconciliation of previous adopted Financial Statements to IFRS Standards at the date of transition.

- Reconciliation of profit for the latest financial statements presented in previous year.

We will surely bring to you with the other IFRS with thorough understanding.

In case of any queries or requirements contact

Team

Compliance Arena

info@compliancearena.in

8447773833